The 20% rise in oil prices since the beginning of September has put the US shale industry’s hedging programs in a precarious position. The 40 US-focused E&Ps covered in our HedgeAware platform have hedged a greater share of their ongoing oil production volumes for Q4 2017 than any of the previous seven quarters, if not longer. But rising oil prices and a futures market in backwardation threaten the efficacy of the industry’s hedges, rendering many a potential liability. This blog post examines Q3 2017 financial and operational performance as well as hedging positions for Q4 2017 and beyond for 40 E&Ps. The figures presented below are drawn from our interactive HedgeAware platform, which incorporates data from Q3 2017 financial disclosures and investor presentations to present detailed oil and gas hedging intelligence. For more information about HedgeAware and the full list of covered companies, please visit www.petronerds.com/hedgeaware. Although this blog post looks at hedging positions in aggregate for all 40 companies, HedgeAware enables users to drill-down by individual company or companies, product type (oil, gas, ngls), date, hedge type, and much more.

Q3 2017 Performance Overview

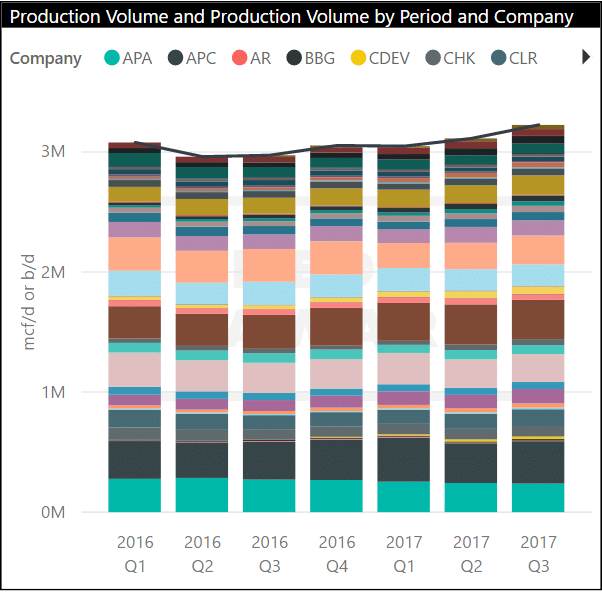

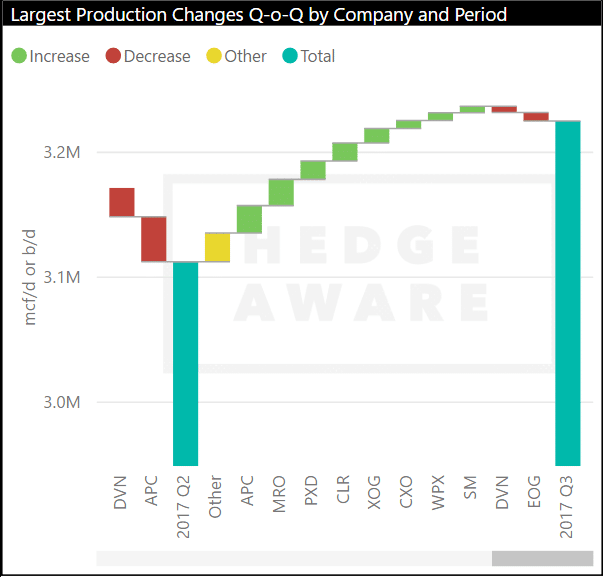

The 40 E&Ps tracked by HedgeAware increased aggregate oil production by 113 kbd (thousand barrels per day), an increase of 3.6%, from Q2 2017 to Q3 2017 (Figure 1). MRO (Marathon), PXD (Pioneer), and CLR (Continental) were among the largest contributors to group’s growth, while DVN (Devon) and EOG both saw slight drops in production volumes (Figure 2).

Figure 1. Oil Production Volumes (b/d)

Source: HedgeAware

Figure 2. Largest Changes in Q-o-Q Oil Production Volumes, by Company (b/d)

Source: HedgeAware

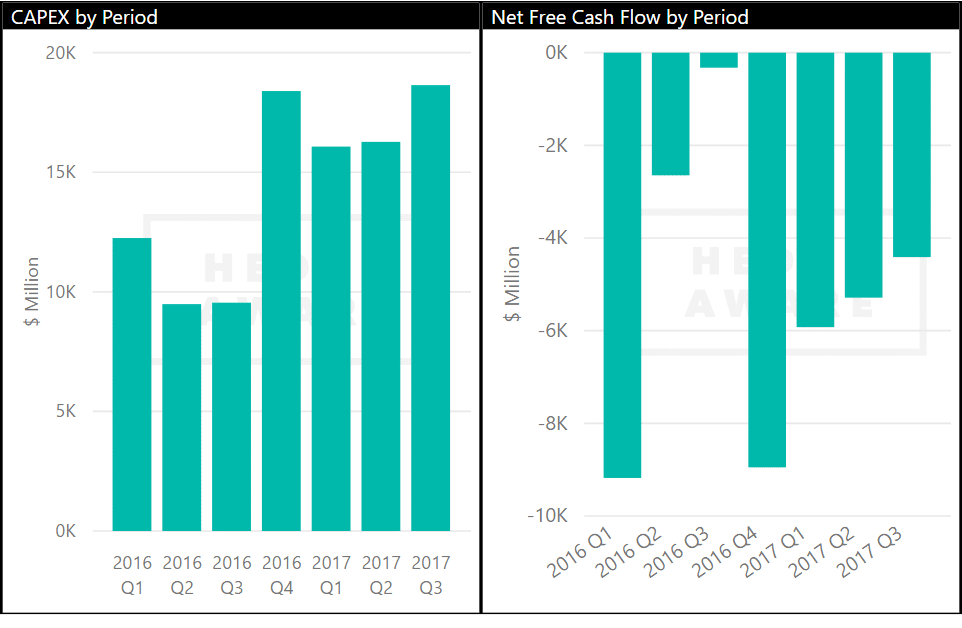

The group’s CAPEX rose by over $2 billion from Q2 2017 to $18.6 billion. This is the second consecutive quarter in which these companies have increased CAPEX. Meanwhile, free cash flow improved for the third quarter in a row, rising from -$5.3 billion to -$4.4 billion.

Figure 3. CAPEX and Free Cash Flow for 40 E&Ps

Source: HedgeAware, financial data via Morningstar

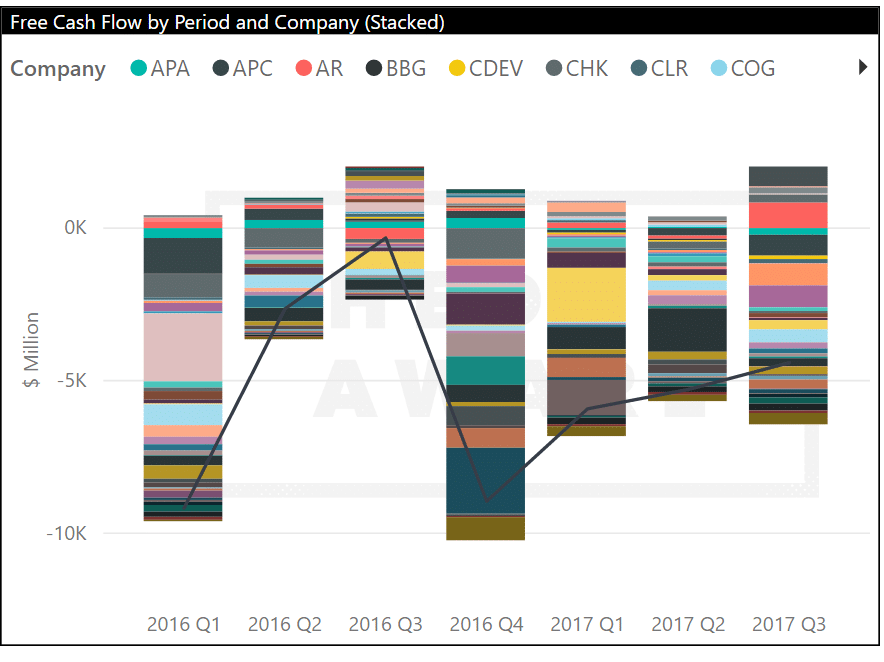

AR (Antero Resources), primarily a natural gas producer, and QEP provided the largest positive contributions to the group’s free cash flow position. It should be noted that a monetization of financial derivatives and proceeds from an asset sale (net CAPEX reduction) contributed to the FCF positions of these two companies, respectively. Without said contributions, aggregate net free cash flow for the 40 companies would have declined from Q2 to Q3.

Figure 4. Free Cash Flow by Company

Source: HedgeAware, financial data via Morningstar

Past Hedging Performance

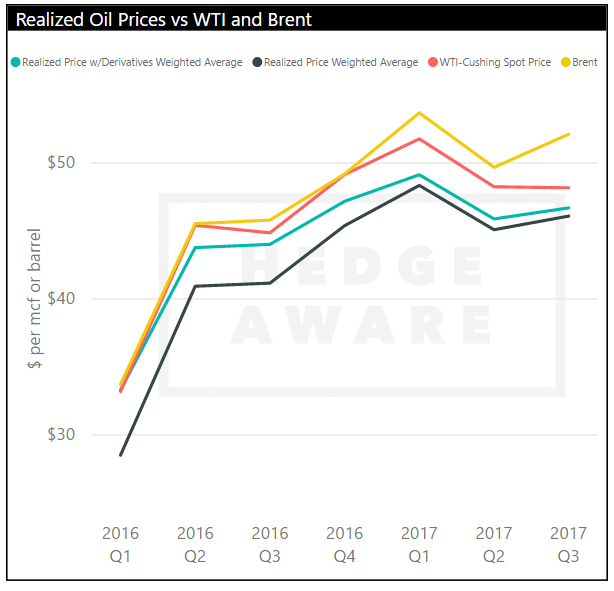

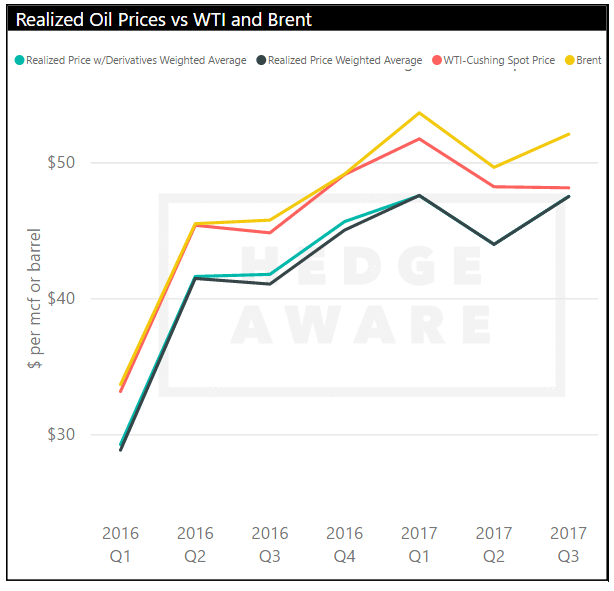

Realized per barrel sales prices with and without the impact of derivatives picked up slightly in Q3, even as WTI remained flat from Q2 to Q3. The primary factor behind this is the widening of the WTI-Brent spread. The first chart in Figure 5 below shows realized sales prices for combined domestic and international sales against WTI and Brent. The second chart displays only international sales. Note how the green and black realized sales price lines run nearly parallel to the yellow Brent spot price line, indicating sales prices tied to the Brent benchmark. Although international sales account for slightly less than 20% of these 40 companies’ production volumes, the sharp divergence in domestic and international pricing was enough to bump up overall sales prices Q-o-Q.

Figure 5. Realized Oil Sales Prices vs WTI and Brent. First Chart Includes Sales Prices from US and Intl Sales, Second Shows Only Intl Sales.

Source: HedgeAware. Where companies do not report derivative impact on a per unit basis, the price without derivatives is used for both categories. Therefore, the aggregated derivative impact in Figure 5 may differ from the average of the group in Figure 6.

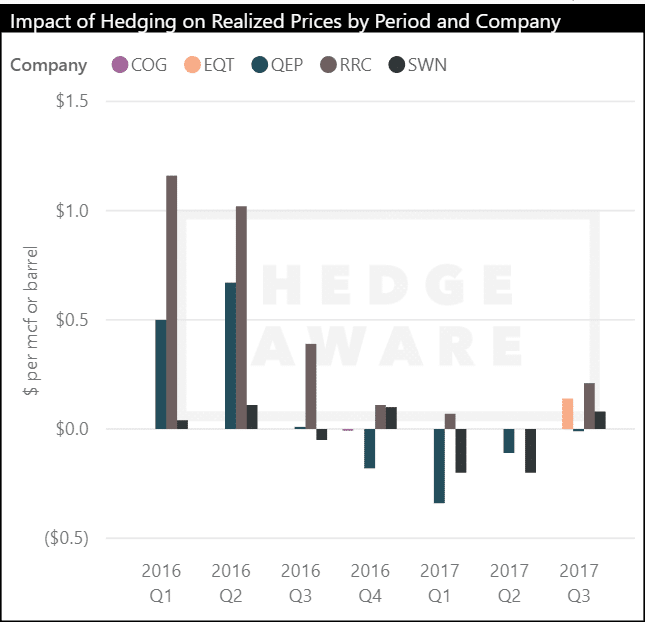

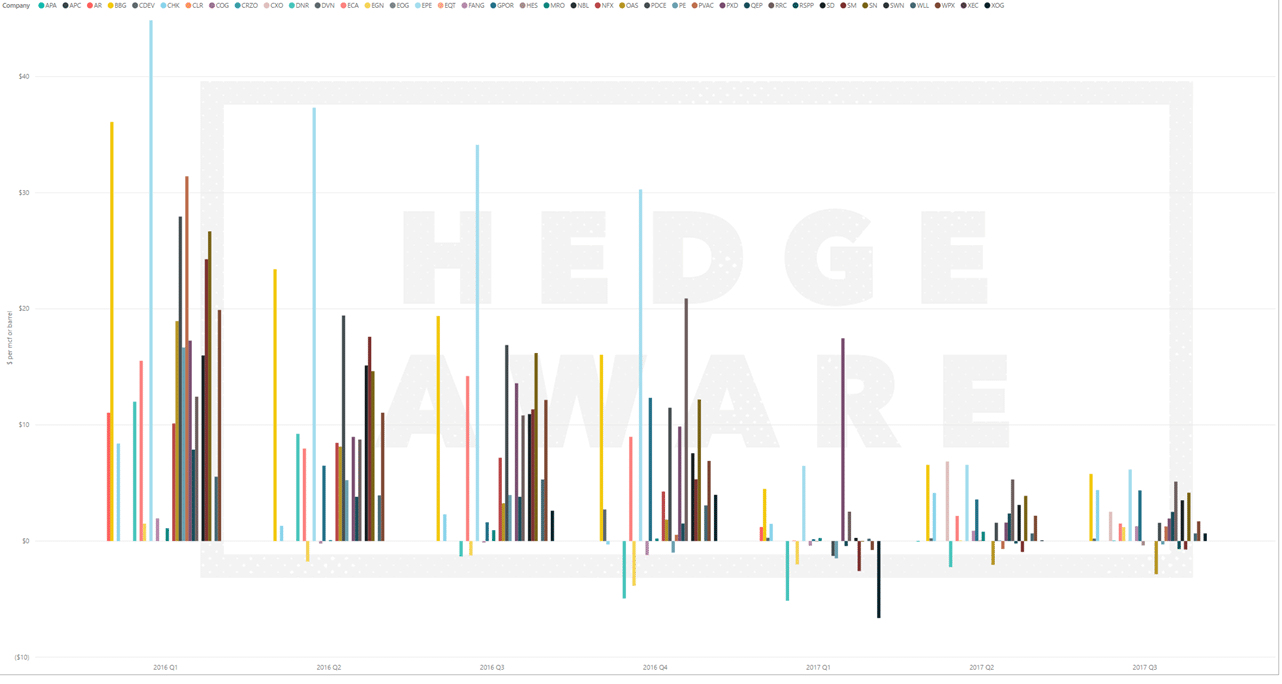

The following chart shows the derivative impact on realized oil prices for companies that specifically break out derivative impacts on a per unit basis. Derivatives are providing a far smaller impact on realized prices than they were a year ago when $10/b gains were not uncommon. Nevertheless, derivatives provided a positive impact for nearly all reporting companies in Q3. EPE led the pack with a positive derivative impact of $6.16/b.

Figure 6. Impact of Hedging on Realized Oil Price

Source: HedgeAware

Expect things to look bleaker in Q4, however, as we explain below.

Q4 Oil Hedging Outlook

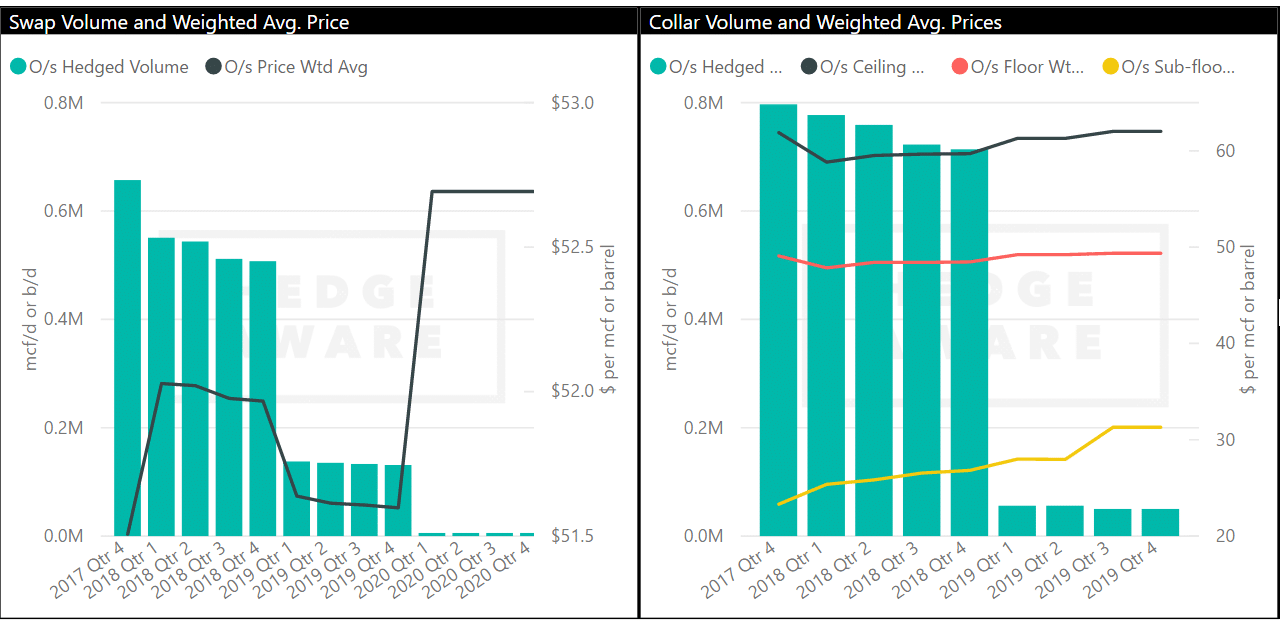

The 40 companies we cover entered Q3 with a volume weighted average swap price of $52.40 and a volume weighted average collar floor of $49.10. WTI, the benchmark to which nearly all US based E&Ps base their hedges, averaged $48.16/b in Q3. Therefore, both hedging mechanisms provided a positive impact over the course of Q3. The Q3 derivative impacts depicted in Figure 6, in which most companies fell into a range of +$0/b to +$5/b, makes sense given this context ($4/b benefit from swaps, $1/b from collars). The problem the industry now faces is that oil prices have risen beyond the prices at which they were hedged on September 30 (or later for those who reported subsequent modifications to hedging positions) entering Q4.

The group has hedged 657 kbd with swaps at a volume weighted average price of $51.51/b and nearly 800 kbd in collars with a volume weighted average ceiling of $61.88/b and a floor of $49.09. But oil prices have risen from approximately $50/b in early October to over $57/b as of November 21, 2017. The group’s aggregate swap position at $51.51 has been underwater for much of Q4. Its collars are providing neither a positive nor negative impact at the moment, premiums excluded, as oil prices remain between the floor and ceiling. Derivative pricing has been further complicated by the backwardation of the oil futures market, which prevents companies from locking in future prices above prevailing, present-day market prices.

Figure 7. Aggregate Oil Swap and Collar Positions for 40 Companies Entering Q4 2017 (b/d)

Source: HedgeAware

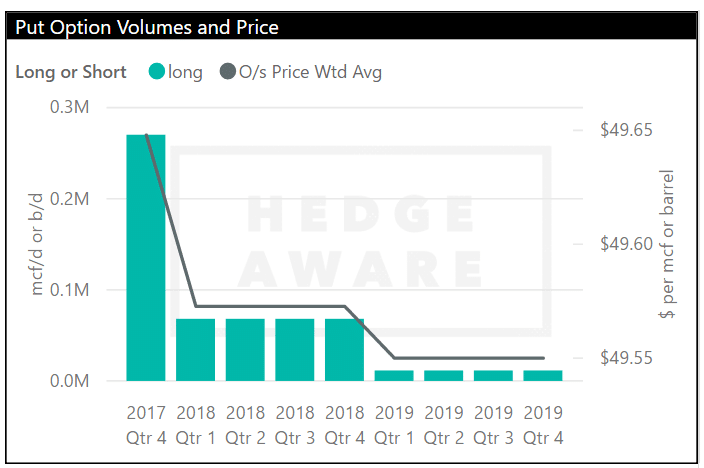

The group has also accumulated a significant long put option position, which provides 270 kbd of downside price protection below $49.65/b. These put options will probably expire out of the money absent a marked drop in crude oil prices over the next six weeks.

Figure 8. Gross Long Put Option Positions

Source: HedgeAware

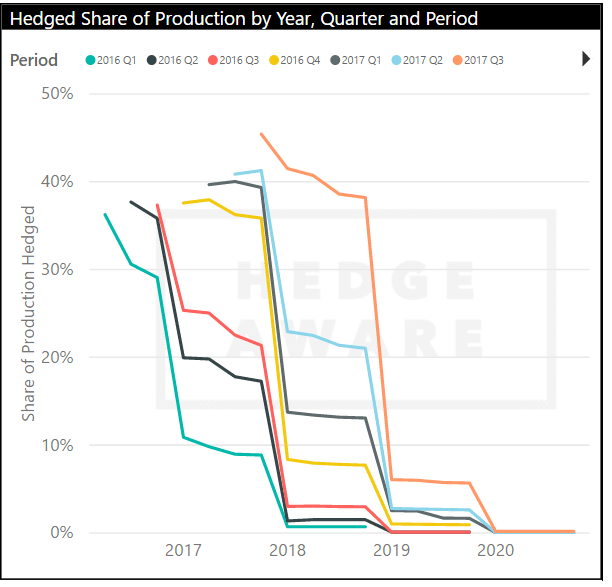

We said earlier that producers were more heavily hedged now than since at least Q1 2016. Figure 9 below illustrates that statement, depicting future swap and collar volumes as a share of that period’s production volumes. The orange line to the far right, labelled 2017 Q3 in the legend, shows that the group has hedged 45.43% of Q3 production volumes in Q4, the highest prompt period level since at least the start of 2016. The upward shifts of the curves over time indicate that producers have grown increasingly more aggressive with their hedging positions.

Figure 9. Outstanding Swap and Collar Volumes as a Share of Production

Conclusion

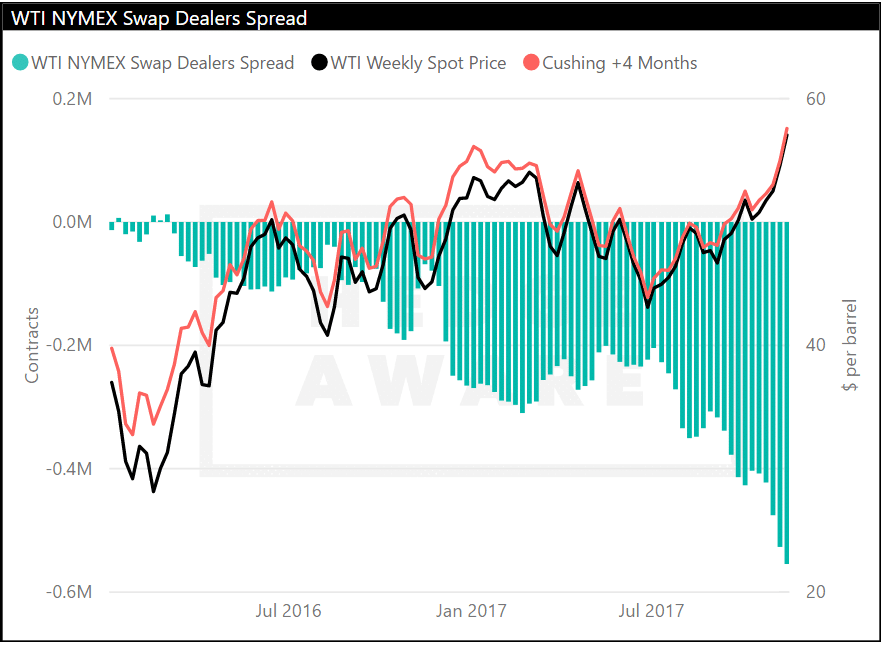

It is unfortunate for the industry that just as they ratchet their hedges to their highest level in years, a rise in oil prices puts many of these positions in the red. More companies than not may well lose money on their oil hedging positions this quarter, barring adjustments to derivative portfolios or a dip in prices. But, those adjustments may be occurring. CFTC data presented in Figure 10 shows that swap dealers have taken on their largest short position in years. Movements in the position of swap dealers are considered to be a proxy for hedging activity among E&Ps. So, as oil prices have risen rapidly in recent weeks, swap dealers, often on behalf of the industry, have sold increasingly large numbers of futures contracts to lock in these rising prices. Doing so does not come without a cost and companies could be taking a loss on any existing positions they may be closing that are currently underwater. However, this data suggests that companies are actively reworking their portfolios to position themselves for a higher price environment, even if they must incur losses in the short-term. The real risk is that prices continue to rise and these producers are forced to play catch-up or cut their losses.

Figure 10. CFTC Swap Dealers Net Position – Swaps and Options Combined